Over last Summer someone said that when China sneezes the world catches a cold.

I believe that China has gone beyond sneezing and it has a "flu", which means the rest of the world is about to catch pneumonia.

While all media outlet are focusing on China as it was an isolated problem kindly note that the Chinese economic slowdown and the cover up over real economic performance is ONLY one of the several problems currently plaguing the global economy: distorted monetary policies, failed monetary experiments like the EUR, geopolitical risk in the Middle East just to name a few.

For the purpose of this writing though we will focus only on the reasons why an economic slowdown of the Chinese economy is so impactful on the global economy.

In statistical terms the picture below gives you an idea of the commodity consumption of China in 2015:

China has been fueling an unprecedented INVESTMENT-LED infrastructure expansion that has been prompting an economic expansion across all emerging markets.

Merely as an example Australia benefited greatly from the Chinese economic expansion by exporting its iron ore and adding capacity along its way.

To understand the value of 1% of economic Chinese below are the GDP rankings based on PPP valuation.

Since 2008 China has been contributed the largest share of global growth, the IMF has been projecting that China would contribute double the global GDP growth than the USA. And China and the USA together are expected to generate as much growth output as the rest of the world put together with the third largest contributor being the European Union if taken as a WHOLE.

BUT the game is now coming to an end. Or better yet, the bluff has been called and as China tries to make a transition into a middle income country global economy is about to face significant headwind.

The official GDP numbers published by the Chinese authorities keep on being revised down, nobody believes the official numbers anymore and everybody tries to estimate the REAL value of the Chinese GDP.

Estimates on the street depending on the outlets range from -1% to +2.5%.

Indicators confirming the Chinese slowdown lie in the amounts of commodities truly absorbed by the economy. On the ground witness confirm that China is no longer absorbing the same amount of commodities as before, in many cases output production is cut.

I.e. Chinese steel is now dumped on the international markets decreasing price.

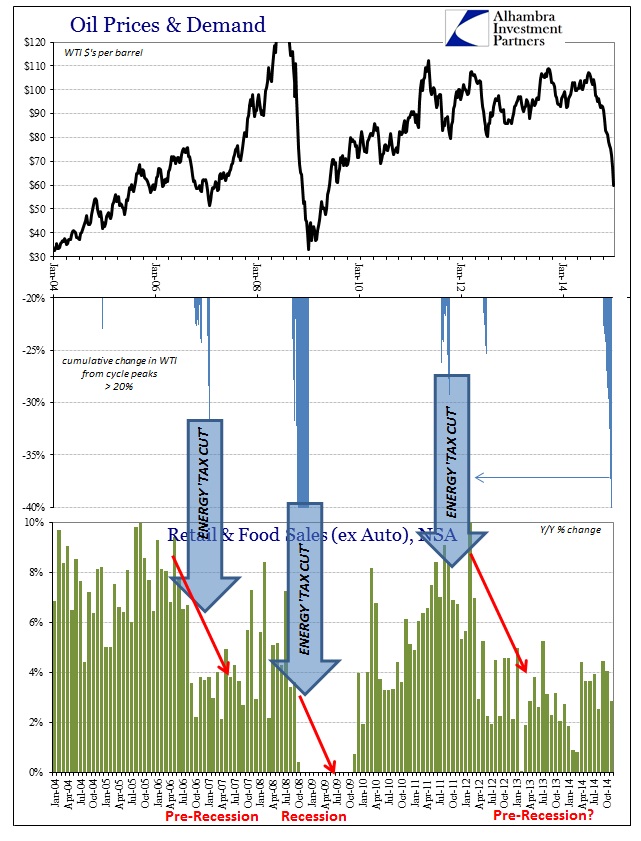

Kindly note that as recently as yesterday the oil contango widened signaling a further oversold sentiment. The contango in the front end of WTI crude forward curve widened to the highest level since 2008. This signals a significant sell-off in the physical market as demand is weak and inventory levels are high. (for a definition of "contango" kindly follow this link)

The most affected by the slowdown will be the commodity exporters that used to supply China with their raw materials:

It is likely that one of the hardest hit will be the FTSE where a large portion of the commodity stocks are listed.

As shared at the beginning of this writing the Chinese slowdown is ONLY one of the ingredients bound to push the global economy into a bear market. We have strongly believed that we needed just a trigger to call in the bluff of the equity markets and we have gone many potential triggers in place.

I am afraid the China related first trigger have just being pulled.

The financial markets will now begin a long and painful process of deleveraging that will once again point out the fragility of our global financial systems and staggering amount of non serviceable debt accumulated across all markets.

More to it on our next post.

I believe that China has gone beyond sneezing and it has a "flu", which means the rest of the world is about to catch pneumonia.

While all media outlet are focusing on China as it was an isolated problem kindly note that the Chinese economic slowdown and the cover up over real economic performance is ONLY one of the several problems currently plaguing the global economy: distorted monetary policies, failed monetary experiments like the EUR, geopolitical risk in the Middle East just to name a few.

For the purpose of this writing though we will focus only on the reasons why an economic slowdown of the Chinese economy is so impactful on the global economy.

In statistical terms the picture below gives you an idea of the commodity consumption of China in 2015:

China has been fueling an unprecedented INVESTMENT-LED infrastructure expansion that has been prompting an economic expansion across all emerging markets.

Merely as an example Australia benefited greatly from the Chinese economic expansion by exporting its iron ore and adding capacity along its way.

To understand the value of 1% of economic Chinese below are the GDP rankings based on PPP valuation.

Since 2008 China has been contributed the largest share of global growth, the IMF has been projecting that China would contribute double the global GDP growth than the USA. And China and the USA together are expected to generate as much growth output as the rest of the world put together with the third largest contributor being the European Union if taken as a WHOLE.

BUT the game is now coming to an end. Or better yet, the bluff has been called and as China tries to make a transition into a middle income country global economy is about to face significant headwind.

The official GDP numbers published by the Chinese authorities keep on being revised down, nobody believes the official numbers anymore and everybody tries to estimate the REAL value of the Chinese GDP.

Estimates on the street depending on the outlets range from -1% to +2.5%.

Indicators confirming the Chinese slowdown lie in the amounts of commodities truly absorbed by the economy. On the ground witness confirm that China is no longer absorbing the same amount of commodities as before, in many cases output production is cut.

I.e. Chinese steel is now dumped on the international markets decreasing price.

Kindly note that as recently as yesterday the oil contango widened signaling a further oversold sentiment. The contango in the front end of WTI crude forward curve widened to the highest level since 2008. This signals a significant sell-off in the physical market as demand is weak and inventory levels are high. (for a definition of "contango" kindly follow this link)

The most affected by the slowdown will be the commodity exporters that used to supply China with their raw materials:

- Australia: China accounts for 1/3 of all Australian exports;

- Sub Saharan countries: 1/8 of total exports goes to China; but the impact will be concentrated since five countries account for three-quarters of all of Africa’s exports to China: Angola, the Democratic Republic of the Congo, Equatorial Guinea, Republic of Congo, and South Africa.

- Latin America: China has surpassed the US as the most important trading partner for Latin America.

Next in line to be affected are the European luxury brands that have counted on the Chinese market for a silver-lining in the face of a general slow growth global economy.

The EU is China’s largest trading party, and China is the second-largest trading partner of the EU after only the US. The Chinese slowdown is therefore reflected in the profit warnings issued by European companies such as Burberry and BMW as their sales in China slows down.

Last but not least FINANCIAL MARKETS will be dragged down by the evident slowdown.

It is likely that one of the hardest hit will be the FTSE where a large portion of the commodity stocks are listed.

As shared at the beginning of this writing the Chinese slowdown is ONLY one of the ingredients bound to push the global economy into a bear market. We have strongly believed that we needed just a trigger to call in the bluff of the equity markets and we have gone many potential triggers in place.

I am afraid the China related first trigger have just being pulled.

The financial markets will now begin a long and painful process of deleveraging that will once again point out the fragility of our global financial systems and staggering amount of non serviceable debt accumulated across all markets.

Opportunities for profits available in this environment:

- Low risk: algorithmic based spread arbitrage on selected commodities and fx pairs across multiple exchanges;

- Medium risk: transactional funding of agricultural based commodities.

More to it on our next post.